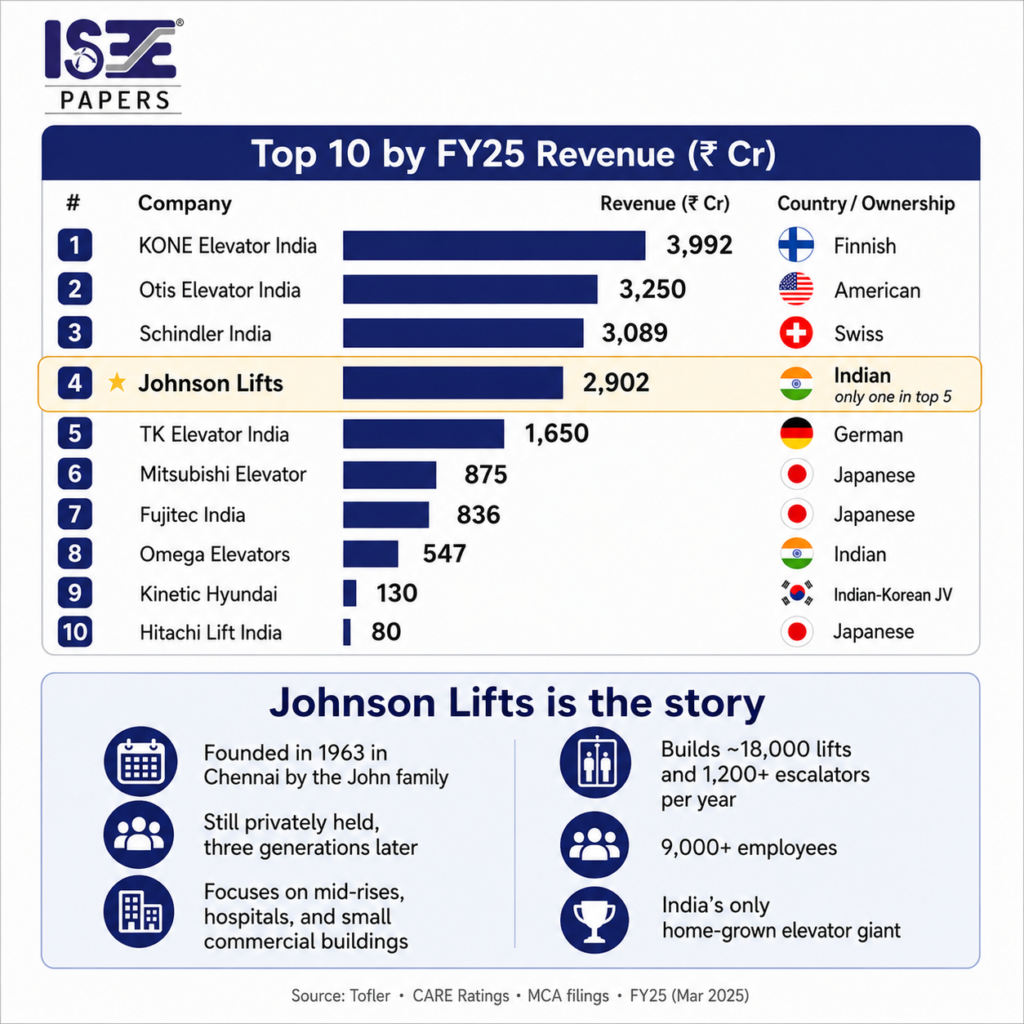

Top Lift Companies in India by Revenue FY25 | ISEE Papers

Market Analysis | Vertical Transportation India’s Elevator Market: Foreign Revenue Leaders, Indian Installation Strength Four of India’s top five lift makers by FY25 revenue are foreign-owned. But the company leading by units installed is Indian. That difference reveals how layered India’s elevator market really is. By ISEE Papers Editorial Desk Vertical Transportation Industry FY25 Revenue Analysis 4 of India’s top 5 lift makers are foreign-owned. Finland. USA. Switzerland. Germany. The only Indian company in the top five is Johnson Lifts, a Chennai family business founded in 1963. ₹16,000 Cr Estimated size of India’s elevator market. ~85% Market concentration among just five companies. ₹14,232 Cr Combined FY25 revenue of the top five companies. India’s vertical transportation market is expanding with the country’s skyline. From metro stations and hospitals to malls, offices, airports, and residential towers, elevators are now central to how modern India moves. But behind this growth lies a striking market pattern. The highest revenue positions are largely held by global companies, while one of the strongest installation stories belongs to an Indian manufacturer. According to FY25 revenue data sourced from Tofler, CARE Ratings, and MCA filings, nearly 85% of India’s estimated ₹16,000 crore elevator market is concentrated among just five companies. Advertisement Place leaderboard ad banner here, recommended size: 970 × 250 or responsive display ad. The Top 10 Lift Makers in India by FY25 Revenue The revenue table shows a clear global presence at the top of India’s elevator market. KONE Elevator India leads by FY25 revenue, followed by Otis Elevator India, Schindler India, Johnson Lifts, and TK Elevator India. # Company FY25 Revenue Country / Ownership 1 KONE Elevator India ₹3,992 Cr Finnish 2 Otis Elevator India ₹3,250 Cr American 3 Schindler India ₹3,089 Cr Swiss 4 Johnson Lifts Only Indian in Top 5 ₹2,902 Cr Indian 5 TK Elevator India ₹1,650 Cr German 6 Mitsubishi Elevator ₹875 Cr Japanese 7 Fujitec India ₹836 Cr Japanese 8 Omega Elevators ₹547 Cr Indian 9 Kinetic Hyundai ₹130 Cr Indian-Korean JV 10 Hitachi Lift India ₹80 Cr Japanese Advertisement Place in-article display ad here, recommended size: 728 × 90 or responsive ad unit. Revenue Leadership vs Installation Leadership One of the most interesting parts of India’s elevator market is that leadership changes depending on what is being measured. KONE leads by revenue. Johnson Lifts leads by units installed. This makes the Indian market more layered than a simple revenue ranking. Global brands dominate much of the premium revenue pool, especially in high-rise buildings, commercial towers, luxury developments, and large infrastructure projects. Indian manufacturers, meanwhile, continue to hold strong ground across everyday vertical mobility needs such as mid-rise residential buildings, hospitals, smaller commercial buildings, and regional infrastructure. In short, India installs a large number of Indian lifts, but pays higher values for many foreign-owned systems. Johnson Lifts: India’s Home-Grown Elevator Giant Johnson Lifts stands out because it is the only Indian company among the top five by FY25 revenue. Founded in Chennai in 1963 by the John family, the company remains privately held and family-led three generations later. Unlike some global players that are closely associated with landmark towers and premium commercial projects, Johnson Lifts has built its scale through a much wider base of practical Indian demand. Founded in 1963 Built in Chennai by the John family. Three generations Still privately held and family-led. ~18,000 lifts per year Along with 1,200+ escalators built annually. 9,000+ employees One of India’s largest home-grown elevator companies. The company’s strength lies in the places where India’s elevator requirement is most consistent: mid-rise buildings, hospitals, small commercial properties, apartment blocks, and institutional projects. Its market position is not built only on visibility. It is built on reach, service, installation volume, and a deep understanding of Indian building conditions. Sponsored Placement Place brand story, product spotlight, or native ad block here. A Market Dominated by Global Ownership Eight of the top 10 companies are foreign-controlled or joint ventures. Only two, Johnson Lifts and Omega Elevators, are purely Indian. That does not make the foreign presence unusual. Elevators are a technology-heavy sector requiring advanced safety systems, control mechanisms, testing standards, manufacturing precision, maintenance networks, and long-term service reliability. Global players bring decades of experience, established technology platforms, and international project credibility. Otis, for instance, has been present in India since 1953. Globally, it is associated with iconic structures such as the Empire State Building, where Otis elevators were installed in 1931. TK Elevator is known for innovations such as MULTI, the world’s first rope-less elevator system. These companies bring global engineering heritage into India’s rapidly urbanizing built environment. But the Indian story is equally important. Johnson Lifts shows that domestic manufacturers can compete at scale, especially when they build for Indian conditions, Indian price expectations, Indian service needs, and Indian building typologies. Foreign brands lead much of the revenue table. Indian companies continue to power a large part of everyday lift installation. What This Means for India’s Vertical Transportation Industry India’s elevator market is not just about who sells the most expensive systems or who installs the most units. It reflects a broader reality of the country’s infrastructure growth. Premium urban projects continue to favour global brands. Mass-market installation volume continues to create room for strong Indian companies. Both segments are growing, but they follow different economics. This is why the gap between revenue leadership and unit leadership matters. It shows that India’s vertical transportation industry is not one market. It is many markets operating together: luxury towers, affordable housing, hospitals, railway and metro infrastructure, malls, offices, small commercial buildings, public projects, and regional real estate. Each of these demands different price points, service models, engineering requirements, and brand expectations. Advertisement Place mid-article ad banner here, recommended size: 300 × 250, 336 × 280, or responsive ad unit. The Bigger Question for Indian Manufacturing The elevator industry raises an important question for Indian manufacturing: can India produce more home-grown companies that lead not only by volume, but also by revenue, technology, and premium positioning? Johnson

The “Net-Zero” Elevator

The “Net-Zero” Elevator The concept of the Net-Zero Elevator marks a shift from vertical transportation being a “power drain” to becoming a “power plant.” In modern green buildings, elevators can account for 2% to 10% of total energy consumption. Achieving “Net-Zero” in this sector involves a combination of energy generation, ultra-efficient hardware, and AI-driven idle management. 1. Core Technology: The Regenerative Drive The cornerstone of a Net-Zero system is the Regenerative Drive. Traditional elevators use resistors to dissipate energy as heat when the motor acts as a brake. A regenerative system captures this mechanical energy and converts it into electricity. How it Works: Energy is generated in two scenarios: When a heavily loaded car travels down (gravity does the work). When an empty or lightly loaded car travels up (the counterweight pulls it up). Efficiency Gain: These drives can recover up to 30% to 40% of the energy used by the elevator, feeding it back into the building’s electrical grid to power lights, HVAC, or other machinery. 2. Eliminating the “Vampire Draw”: Standby Efficiency Elevators spend approximately 80% of their lifespan in standby mode. Even when not moving, they consume power for lighting, fans, displays, and controllers. Sleep Mode: Modern systems use “deep sleep” protocols that deactivate non-essential electronics when the lift is idle for more than 5 minutes. LED Transition: Replacing traditional incandescent or halogen cab lighting with motion-sensor LEDs reduces cab energy use by 50% to 75%. Smart Dispatching: AI algorithms (Destination Control Systems) group passengers going to the same floor, reducing the total number of “starts” and “stops,” which are the most energy-intensive parts of a trip. 3. Hardware Innovations: Weight & Friction Reducing the physical energy required to move the cab is essential for reaching net-zero goals. Carbon Fiber Hoisting: Conventional steel cables are heavy. Switching to carbon fiber tapes (like Otis Compass or KONE UltraRope) reduces the moving mass by up to 90% in high-rise buildings, drastically lowering the torque required from the motor. Permanent Magnet Motors: Gearless motors using permanent magnets are roughly 25% more efficient than traditional induction motors and require no oil, reducing environmental waste. 4. Integration with Building Renewables A “Net-Zero” elevator is rarely a closed loop; it is part of a Smart Grid ecosystem. Solar Integration: In B2C residential settings, elevators are being paired with rooftop solar arrays and lithium-ion battery buffers. The batteries store solar power during the day and regenerative energy during travel, allowing the elevator to run entirely “off-grid” during peak hours or power outages. Microgrids: By 2026, the trend is moving toward Building Management Systems (BMS) that treat the elevator as a flexible load, slowing down travel speeds slightly during peak grid demand to balance the building’s total energy footprint. 5. Summary of Net-Zero Impact Feature Energy Impact Sustainable Benefit Regenerative Drive +30% to 40% recovery Feeds the building grid LED & Sleep Mode -80% standby power Reduces “Vampire” load Carbon Fiber Ropes -15% operational power Reduces structural load AI Dispatching -20% trip frequency Extends equipment life Conclusion Sustainability in the VT industry is no longer just about using less electricity; it is about energy harvesting. The Net-Zero Elevator is achievable today by combining regenerative hardware with AI-managed software, ultimately turning every vertical trip into a contribution to the building’s carbon-neutral goals. This article is published for informational and editorial purposes only. Views expressed may not reflect those of ISEE Papers. We do not guarantee accuracy or completeness. For full details, please read our complete disclaimer here: https://iseepapers.com/isee-papers-website-disclaimer/