FY26 Pre-Sales Show India’s Listed Real Estate Developers Are Entering a Scale Phase

FY26 has closed on a strong note for India’s listed real estate developers. Despite higher borrowing costs, global uncertainty and a cautious economic environment, the country’s residential real estate market has continued to show remarkable strength.

The latest pre-sales numbers underline one clear trend: India’s organised real estate players are not merely surviving market cycles. They are scaling faster, consolidating demand and strengthening their position across key housing markets.

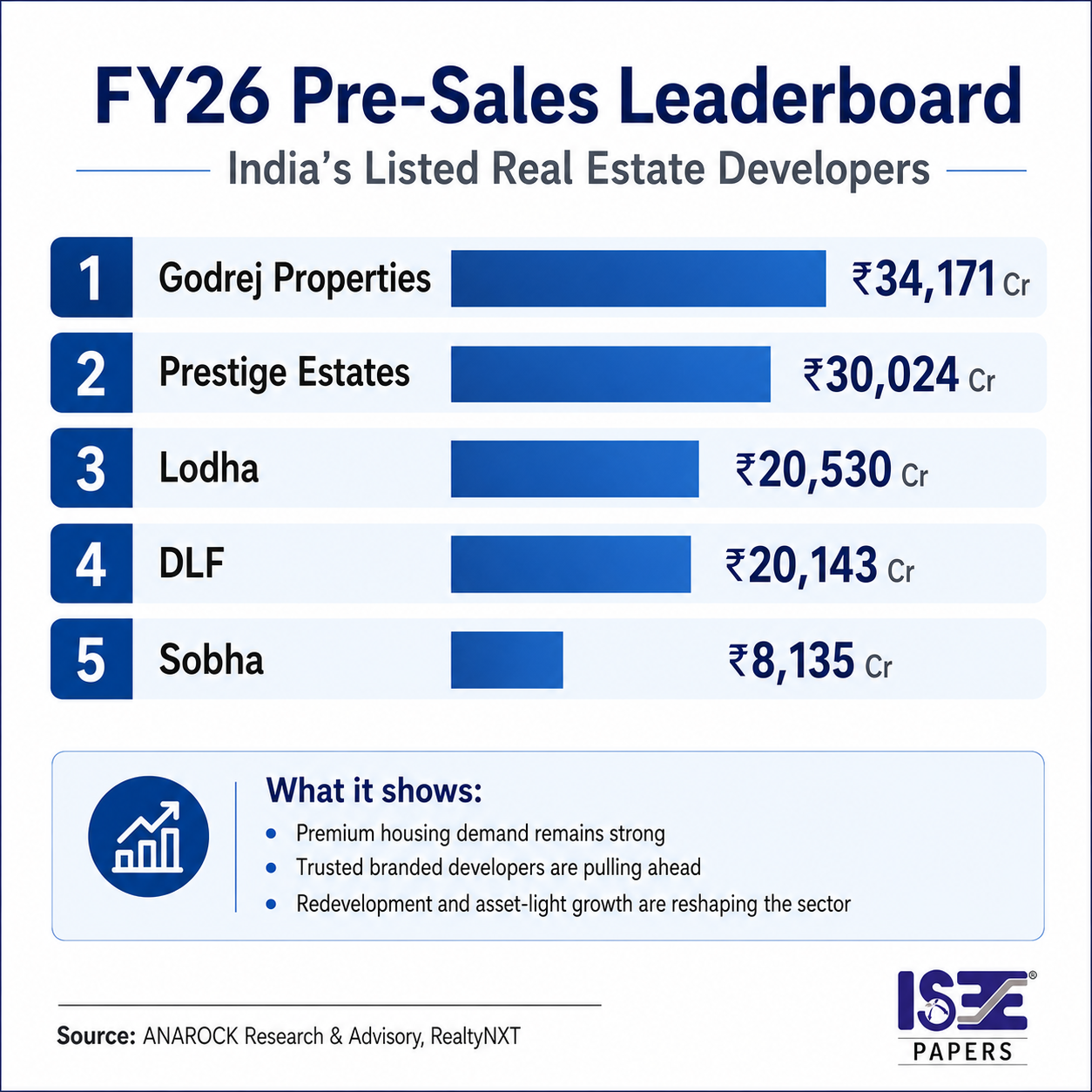

According to data from ANAROCK Research & Advisory and RealtyNXT, Godrej Properties led the FY26 pre-sales leaderboard with ₹34,171 crore, followed by Prestige Estates at ₹30,024 crore. Lodha recorded ₹20,530 crore, DLF stood at ₹20,143 crore, while Sobha reported ₹8,135 crore.

FY26 Pre-Sales Leaderboard

Godrej Properties: ₹34,171 crore

Prestige Estates: ₹30,024 crore

Lodha: ₹20,530 crore

DLF: ₹20,143 crore

Sobha: ₹8,135 crore

Source: ANAROCK Research & Advisory, RealtyNXT

Godrej Properties topping the chart is a significant development. However, the larger story is not only about which developer ranked first. The real story lies in what these numbers say about the changing behaviour of the Indian homebuyer.

Trust Is Becoming the Biggest Differentiator

The Indian homebuyer is becoming more informed, more selective and more cautious about who they buy from. Location, carpet area and pricing still matter, but they are no longer the only deciding factors.

Today, buyers are increasingly looking at the strength of the developer behind the project. They want a builder with a strong balance sheet, a clear delivery record, transparent approvals, regulatory discipline and the ability to complete projects on time.

This shift is one of the biggest reasons listed and organised developers are pulling ahead.

In the past, many buyers were willing to take chances with smaller or lesser-known developers if the price looked attractive. That behaviour is changing. After years of delayed projects, regulatory concerns and financial stress in the sector, buyers are placing a higher premium on credibility.

A trusted brand is no longer just a marketing advantage. It has become a business advantage.

Premium and Luxury Housing Continue to Drive Demand

Another important signal from the FY26 numbers is the strength of demand in premium and luxury housing. Despite higher interest rates and affordability concerns in some segments, demand at the upper end of the residential market has remained strong.

This reflects a broader change in urban India. Buyers with higher incomes are upgrading to larger homes, better locations, stronger amenities and more reliable developers. For many families, the home is no longer seen only as a necessity. It is also a lifestyle decision and a long-term asset.

This has worked in favour of large listed developers, especially those with access to prime land parcels, established brands and the ability to launch high-value projects in major cities.

The Organised Real Estate Gap Is Widening

The gap between organised and unorganised developers is no longer a small difference. It is becoming structural.

Large listed developers have several advantages. They have better access to capital, stronger execution systems, larger land pipelines, better governance and more confidence among buyers, lenders and institutional investors.

This allows them to launch bigger projects, sell faster, raise capital more efficiently and expand across multiple cities.

As a result, the Indian real estate market is gradually moving towards consolidation. Smaller developers may still remain relevant in local markets, but the strongest demand pools are increasingly moving towards branded players.

Redevelopment and Land-Light Growth Are Changing the Game

Beyond pre-sales, another major trend shaping the future of large developers is the shift towards redevelopment and land-light growth models.

Instead of locking large amounts of capital upfront into land acquisition, many developers are exploring joint development agreements, society redevelopment and asset-light partnerships. These models allow faster scaling with lower capital intensity.

Mumbai is one of the biggest examples of this opportunity. The city’s redevelopment market remains massive, and large developers with execution capability, financial strength and brand trust are well placed to benefit from it.

Redevelopment is not just a real estate opportunity. It is also an urban transformation opportunity. Ageing buildings, limited land supply and rising demand for modern housing are creating a strong case for organised players to participate more aggressively in this space.

Infrastructure Is Adding Further Momentum

India’s residential real estate growth is also being supported by infrastructure development. Metro expansion, expressways, airport connectivity, business districts and urban renewal projects are opening new growth corridors across major cities.

Better infrastructure improves accessibility, increases land value and creates new housing demand.

For large developers, this means more opportunities to launch projects in emerging micro-markets. For buyers, it creates greater confidence in long-term value appreciation.

When infrastructure growth combines with trusted developers and rising urban aspirations, the result is a stronger and more organised housing market.

Institutional Capital Is Watching Closely

The performance of listed developers is also important from an investor perspective. Strong pre-sales, disciplined execution and improved governance make the sector more attractive to institutional capital.

Real estate has always been a capital-intensive business. Developers that can demonstrate consistent sales, strong cash flows and project delivery discipline are likely to attract more investor confidence.

This could further strengthen the position of leading listed developers over the next few years.

The Bigger Question: Who Will Lead FY30?

FY26 has given the industry a clear leaderboard. But the bigger question is not only who sold the most this year.

The bigger question is who is building the strongest platform for the next five years.

The developers that can combine land access, execution speed, financial discipline, redevelopment capability and buyer trust will be best positioned to dominate FY30 and beyond.

Godrej Properties has made a strong statement with its FY26 performance. Prestige Estates continues to show scale. Lodha and DLF remain powerful names in premium markets. Sobha continues to stand for quality and delivery in a highly competitive space.

But the next phase of Indian real estate will not be won by sales numbers alone. It will be won by trust, consistency, capital discipline and the ability to deliver across cycles.

FY26 was not a survival year for India’s listed real estate developers.

It was a scale year.

And the race for FY30 has already begun.

Disclaimer: This article is published for informational and editorial purposes only. Views expressed may not reflect those of ISEE Papers. We do not guarantee accuracy or completeness. For full details, please read our complete disclaimer here: ISEE Papers Website Disclaimer